EP57 - California Dream For All Shared Appreciation Loan - Down Payment Assistance

Imagine opening the door to your new home in California, knowing you made it happen with a smart financial move. That's what the California Dream for All program is all about—making homeownership achievable through shared appreciation loans.

You'll get up to $150,000 toward your down payment and won't pay a dime until certain triggers like selling or refinancing kick in. If you're buying for the first time and meet specific income and credit score guidelines, this could be your ticket in.

From single-family homes to condos, learn how this program can help lower initial costs without monthly payments piling on. Plus, for most buyers no mortgage insurance is needed! Ready to dive into details? Let’s unlock that dream together before these limited funds are gone.

SEE IF YOU QUALIFY: CHECK OUR DREAM FOR ALL ELIGIBILITY CALCULATOR

Table Of Contents:

- Unlocking Homeownership with California Dream for All

- How the Shared Appreciation Loan Works

- Eligibility Criteria for Prospective Homebuyers

- Types of Properties Covered by the Program

- Financial Advantages of Choosing Shared Appreciation

- Additional Financial Considerations and Terms

- Navigating the Application Process

- The Long-Term Impact of Shared Appreciation Loans

- Act Now Before Funds Run Out

- Conclusion

Unlocking Homeownership with California Dream for All

Dreaming of owning a home in the Golden State but feeling priced out? The California Housing Finance Agency (CalHFA) might have just the key you need. They're offering eligible borrowers a MASSIVE helping hand—up to $150,000—to help first-time buyers plant roots.

California Dream for All isn't your typical loan. It's more like finding a rich Aunt to help as your silent partner in property investment. It's the best of both worlds. You get the cash to make a sizeable down payment without the stress of monthly payments breathing down your neck.

No Payments or Interest Required

Sounds too good to be true, right? But here's how it works: this second trust deed loan sits patiently waiting while you enjoy homeownership without adding a penny to its tab—no interest accrues and no monthly payments are made.

You live peacefully until certain life events call up that silent partner asking for their share back—and by then, hopefully, you've built enough equity that sharing doesn't sting as much.

Events Triggering Repayment

The day will come when it’s time to settle up—if you sell or refinance your house, or after 30 years of lovingly calling it yours (whichever comes first). There is an EXCEPTION that allows you to refinance one time. You cannot take any cash out of the home equity. It's only to lower your mortgage rate and monthly payment. Still, it's a cool feature.

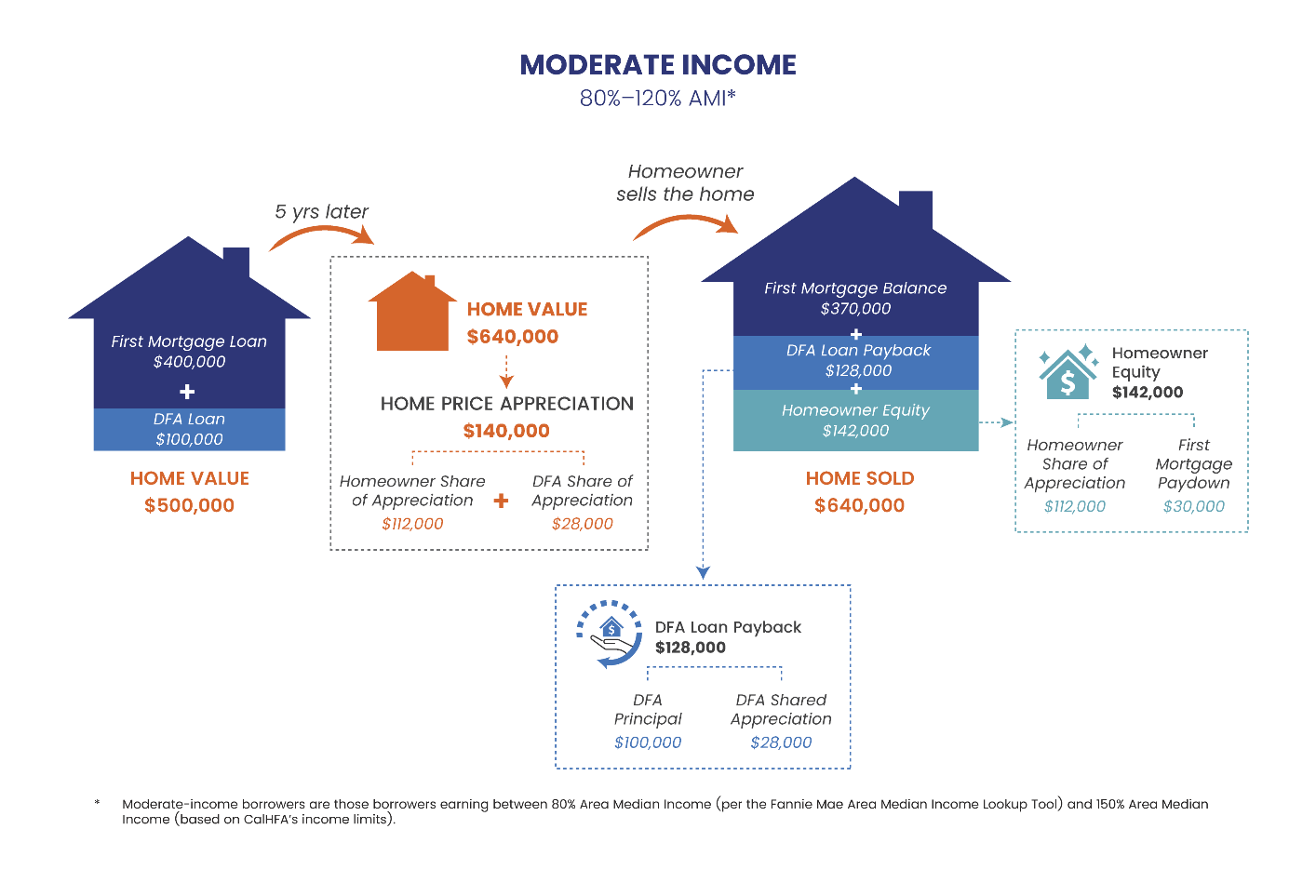

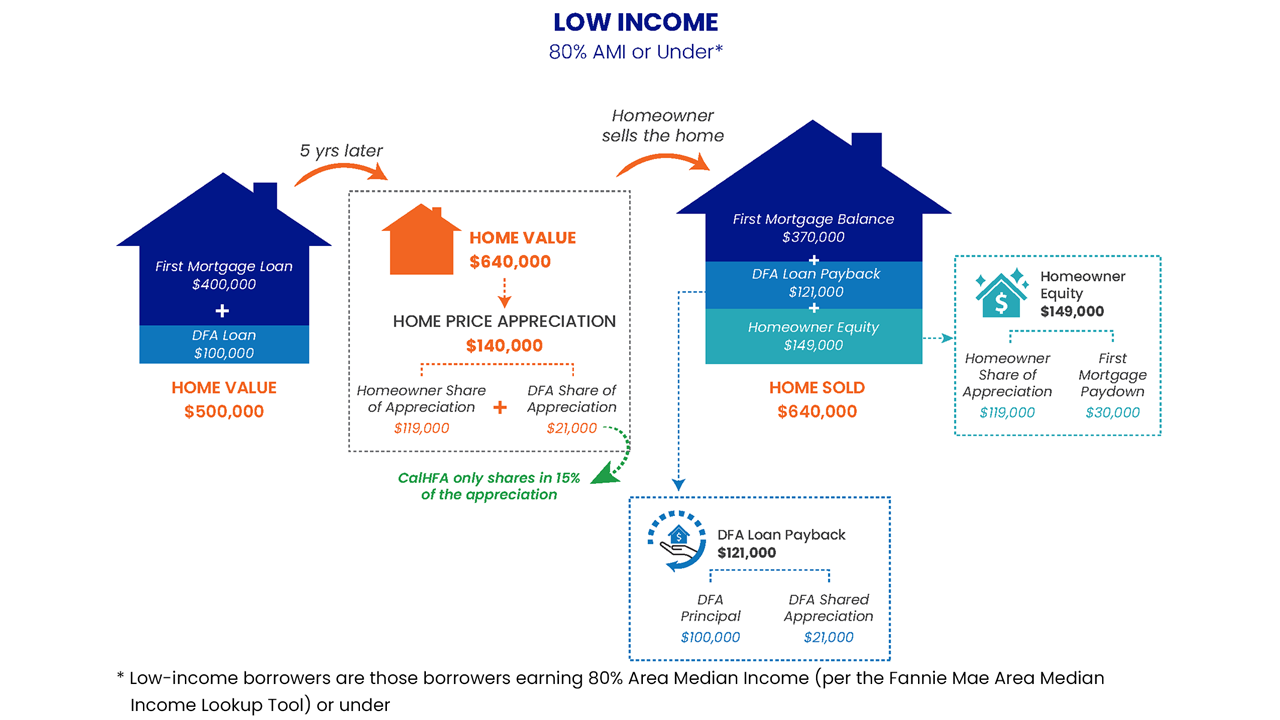

You may be saying this sounds too good to be true. I get a big down payment without making any monthly payments on the extra funds? You would be correct. Once you hit a triggering event, CalHFA will get 20% of any increase in the value of your home in addition to the funds they lent you initially; think of it as giving the State of California a high-five for helping making your home ownership dream a reality with some extra thanks if things went well financially.

And remember, that bump in value is partly thanks to having had the chance at ownership from square one thanks to the Dream For All assistance..

If you're thinking this is the perfect mortgage for you, remember, there are strings attached—there rules about who can snag this deal. First off, you MUST be a first time homebuyer. In addition, there is a new guideline for 2024 that says you must be a first GENERATION home owner. If your parents have owned a home, you're not eligible.

Beyond that, there are income limits that vary by county and your family size.

SEE IF YOU QUALIFY: CHECK OUR DREAM FOR ALL ELIGIBILITY CALCULATOR

How the Shared Appreciation Loan Works

Imagine you've found a way to buy your dream home without paying extra each month. The California Dream for All program makes this possible through its shared appreciation loan, a type of second trust deed that keeps your wallet happy.

No Payments or Interest Required

This isn't your typical loan. Think of it like a silent partner in your home purchase—it's there but doesn't require you to make monthly payments or interest charges. You get the benefit of a chunk of cash to cover a big down payment and closing costs, reducing or eliminating the need for mortgage insurance. All of this keeps your payment down and helps you more comfortably afford a home.

This financial ninja benefactor steps into the shadows and only reappears when specific events occur, such as selling or refinancing your home. You get to enjoy homeownership while postponing payment on part of the cost until later down the road—a pretty sweet deal if you ask me.

Events Triggering Repayment

Certain life changes can mean having to say goodbye to that silent partner —like waving off an old friend who helped you out big time. When you sell, refinance more than one time OR to take cash out, transfer title, no longer use the home as your primary residence or hit 30 years' ownership (whichever comes first), repayment kicks in.

In this case, repayment means the entire loan balance. In addition, you're not just returning what was borrowed; if your home has increased in value, 20% of any increase goes back to the state of California plus the assistance funds they gave you—the initial principal amount—which is fair considering they bet on your house (and future!) too.

But remember: If values haven’t climbed much—or at all—you’re not giving away more than gained from their help. Learn about CalHFA’s terms here.

Eligibility Criteria for Prospective Homebuyers

Defining a First-Time Homebuyer

If you've never owned a home or haven't been on a title in the last three years, guess what? You're considered a first-time buyer. And that's not just us talking—that's straight from CalHFA’s playbook. It means you could be waving goodbye to your landlord sooner than you think.

But it's not just about being new to the game. You need to live in the house too. No renting it out—this is all about making it your own personal slice of California.

And last but not least, you must be a first generation home owner which means "to the best of the homebuyer’s knowledge, their parents do not have any present ownership interest in a home in the United States."

Income and Credit Score Requirements

Your wallet doesn’t have to bulge like a Hollywood mogul’s for this deal, but there are rules. Your income can't go overboard—it needs to play nice with the area median income (AMI). So if big bucks aren’t filling up your bank account yet, don’t sweat; this might be right up your alley.

Credit score-wise, we’re talking minimum FICO scores here folks—and they mean business. If numbers make you dizzy, fear not. CalHFA has counselors who can help steer that credit ship into friendlier waters before diving into homeownership headfirst.

Surely owning four walls and a roof where memories will stack up should feel as epic as finding an extra fry at the bottom of the bag – because let me tell ya, when those keys jingle-jangle in hand for the first time… oh boy.

Types of Properties Covered by the Program

Dreaming of owning a slice of California real estate? The California Dream for All program is like your fairy godmother, turning that dream into reality. But before you start planning where to put your couch, let's break down the details about what kinds of homes are fair game.

If you're eyeing a classic single-family home with a white picket fence, good news: it's on the list. Maybe high-rise living is more your style? Condos make the cut too. For those who fancy flexibility and shared spaces, Planned Unit Developments (PUDs) say 'welcome home'. And if simplicity sings to you, manufactured homes also join this chorus line-up of options—all ready and waiting for first-time buyers looking to plant roots in Cali soil.

The key here isn't just variety; it’s opportunity—your chance to get up close and personal with homeownership without selling an arm or leg. Think less cash upfront thanks to up to $150k towards down payment help. Picture monthly payments that don’t play tug-of-war with every paycheck because guess what—you can skip private mortgage insurance (PMI). So whether it's basking in beachside vibes or thriving urban beats calling out to you, there’s likely a property type under this sun-kissed program waving back at ya.

SEE IF YOU QUALIFY: CHECK OUR DREAM FOR ALL ELIGIBILITY CALCULATOR

Financial Advantages of Choosing Shared Appreciation

Imagine stepping into the world of homeownership and your mortgage giving you a high-five for smart financing. That's what happens when you opt for shared appreciation through California Dream for All. It's like having a silent partner in your investment who only speaks up at payoff time.

Competitive Interest Rates Explained

Say goodbye to private mortgage insurance premiums because they're not required with this gig, which is music to any homebuyer’s ears. Plus, the interest rates? They're as competitive as an Olympic sprinter—tailored to work in favor of different income brackets so that more Californians can cross their own finish lines into homeownership.

This program doesn't just open doors; it practically rolls out the red carpet with financial perks designed to ease the strain on your wallet both now and later. The absence of monthly payments means you can allocate funds elsewhere—maybe towards turning that backyard into a personal oasis or upgrading your kitchen faster than expected.

The real kicker comes when it's time to repay. If property values have risen, 20% of that sweet appreciation plus the initial principal is due—but think about it: You've enjoyed years without payment stress while potentially watching your home’s value climb higher than California redwoods.

No Payments or Interest Required

You heard right. No regular payments loom over your head each month with this assistance loan until certain events trigger repayment—which we'll explore next—making cash flow management smoother than San Francisco fog rolling over Twin Peaks.

Events Triggering Repayment

The day might come when you decide it's time for a change—a sale or refinancing—and that triggers repayment under these terms: cough up 20% of any increase in value alongside what was initially borrowed CalHFA explains. But let's face facts—that increase likely signifies successful investing thanks partly to choosing shared appreciation from jump street.

Step into homeownership with a high-five from your mortgage by choosing shared appreciation—your silent investment partner that speaks up only at payoff time.

Say goodbye to pesky private mortgage insurance and hello to competitive interest rates, tailored for different incomes. This program not only opens doors but rolls out the red carpet of financial perks.

No payments or interest weigh you down monthly with this loan; manage your cash flow smoothly until it's time to repay based on home value increases—a sign of smart investing thanks to shared appreciation.

Additional Financial Considerations and Terms

Refinancing Flexibility with Shared Appreciation Loans

Picture this: You've snagged a shared appreciation loan through the California Housing Finance Agency, you're sitting pretty in your new pad, but now you're eyeing that refinance button. Here's what you need to know. You are limited to only one refinance without triggering repayment. You are not able to take cash out of your home equity. A cash out refinance or a second refinance will trigger repayment.

Navigating the Application Process

Meeting Income and Credit Score Benchmarks

The first step in securing a slice of the California Dream is making sure your wallet aligns with expectations. It's like finding out if you're tall enough to ride the roller coaster – exciting but necessary. To tap into CalHFA's shared appreciation help, you'll need to meet certain income benchmarks that vary by region, so check what those figures look like for your desired neighborhood.

Credit score isn't just a number; it’s your financial report card telling lenders how well you play with borrowed money. You'll need a decent FICO score under your belt—think of it as having at least a 'B' in managing debt—to get past this gatekeeper.

Your journey doesn’t end there though. With these numbers crunched and tucked under your arm, take aim at CalHFA's California Dream for All Assistance Program. Here lies up to $150,000 toward down payment help—a boon for any wallet feeling the squeeze from high upfront costs.

The Long-Term Impact of Shared Appreciation Loans

Think about shared appreciation loans as a seesaw in the playground of real estate finance. On one end, you've got your dream home; on the other, financial flexibility. When it's time to sell or refinance your house, that seesaw tips and it’s payback time for the loan's help.

Repaying Your Shared Appreciation Loan

You landed your new pad with up to \$150,000 toward your down payment, thanks to California Dream for All. But remember: there’s no such thing as free lunch—or free money in this case. Selling or refinancing triggers repayment. You're not just giving back what you borrowed but also sharing 20% of your property's increased value over time.

This might sound like a fair deal now—like splitting fries with a friend—but imagine if those fries turned into gold nuggets by dessert. Yes, you’re gaining equity and enjoying homeownership without monthly payments right away—a huge plus when starting out. Yet fast forward some years; property values have likely gone up and so has the slice of appreciation pie CalHFA will want back.

Surely owning is better than renting because every mortgage payment feels like planting seeds in an investment garden—even more so when someone else foots part of the bill upfront. However—and here comes another analogy—if owning a home is akin to running a marathon, then considering long-term impacts like these helps pace yourself financially so that crossing the finish line doesn't cost more than expected.

Act Now Before Funds Run Out

The clock's ticking on an opportunity that's too good to miss. Think of the California Dream for All program as your VIP ticket to homeownership. It's like finding a golden ticket in your chocolate bar, but instead of touring a whimsical factory, you're stepping into the reality of owning your own home.

This isn't just any help with buying a house; it’s up to $150,000 towards making that hefty down payment more manageable. You heard right—no need for cold sweats over draining savings accounts or calling in family favors. And here’s the kicker: this program is about shared success. When it comes time to sell or refinance, you'll pass on 20% of the property appreciation plus what was initially borrowed—not such a high price considering how much you gain upfront.

But remember, funds are limited and waiting could mean watching this chance slip through your fingers like sand at the beach. Others are surely lining up as we speak because let's face it—who wouldn’t want lower monthly payments without private mortgage insurance? So don't be caught daydreaming when action is what will plant you firmly behind your new front door. Learn more about CalHFA programs and see if they can make your dream come true before someone else takes that last spot under California’s sunny skies.

Conclusion

Unlocking your California dream for all, shared appreciation loans offer a path. They put up to $150,000 in your pocket for that down payment.

Dig into the details. Know that you pay nothing until you sell or refinance—then it's 20% of the gain plus what they gave you.

Check yourself against their list. First-time homebuyer? Check. Income and credit score lining up with theirs? Double-check.

Catch this chance while it flies. CalHFA's down payment help won't wait forever; funds are limited and precious like California sunsets.